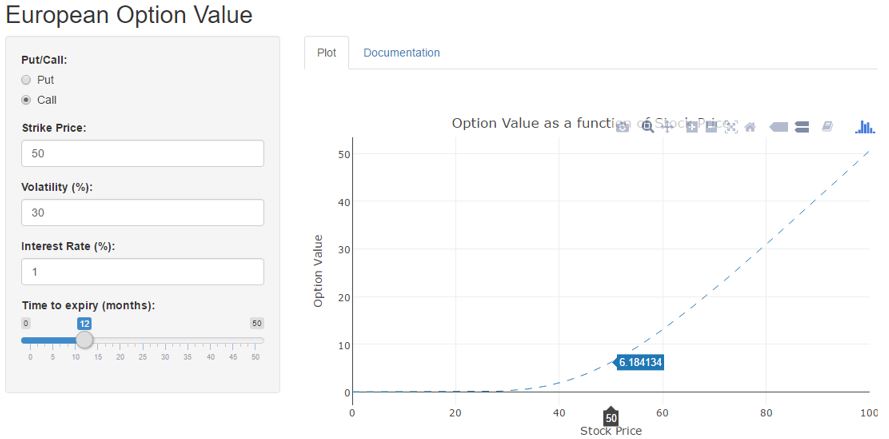

The following code shows how the Black-Scholes Equations are implemented in R.

# the rate, strike price, volatility and time to expiry are supplied as inputs via the Shiny controls

input <- data.frame("rate" = 1, "strike" = 50, volatility = 30, timeToExpiryMonths = 12, putcall = "call")

r <- input$rate / 100

k <- input$strike

v <- input$volatility / 100

t <- input$timeToExpiryMonths / 12

# the application calculates the option values for the range of stock prices from 0 to twice the strike price selected by the user. Here we set the stock price equal to the strike price

s <- k

# code that implements the Black-Scholes Equations

d1 <- (log(s / k) + (r + v ^ 2 / 2) * t) / (v * sqrt(t))

d2 <- (log(s / k) + (r - v ^ 2 / 2) * t) / (v * sqrt(t))

if (input$putcall == "call")

value = s * pnorm(d1) - k * exp(-r * t) * pnorm(d2) else

value = k * exp(-r * t) * pnorm(-d2) - s * pnorm(-d1)

print(paste("Option Value: $", round(value,2)))

[1] "Option Value: $ 6.18"