A Review of Nonlinear Time Series Models

Ran Wang

Contents

TAR: Threshold Autoregressive

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

Model Estimation: Tsay's Approach

SETAR (Self-Exciting Threshold Autoregressive)

SETAR (Self-Exciting Threshold Autoregressive)

STAR (Smooth Transition Autoregressive)

STAR (Smooth Transition Autoregressive)

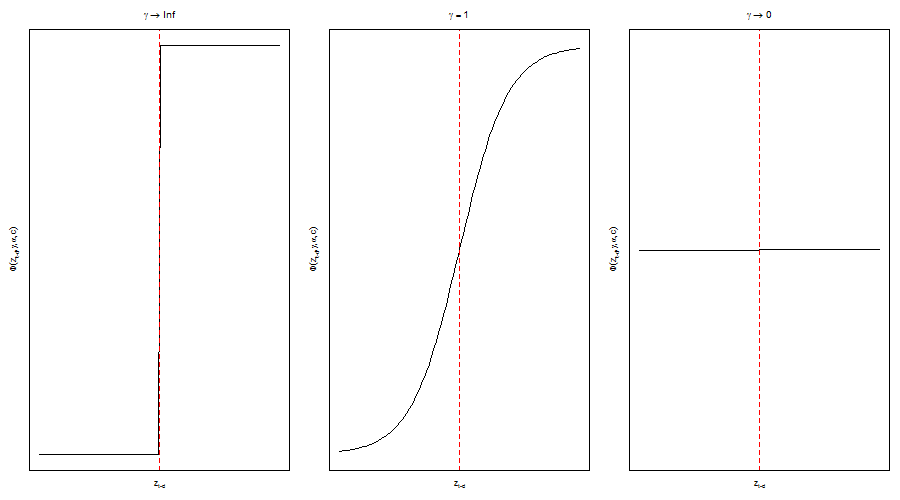

- 1 Logistic STAR:

\[ G(z_t)=\frac{1}{1+e^{-\gamma(z_t-c)}} \]

STAR (Smooth Transition Autoregressive)

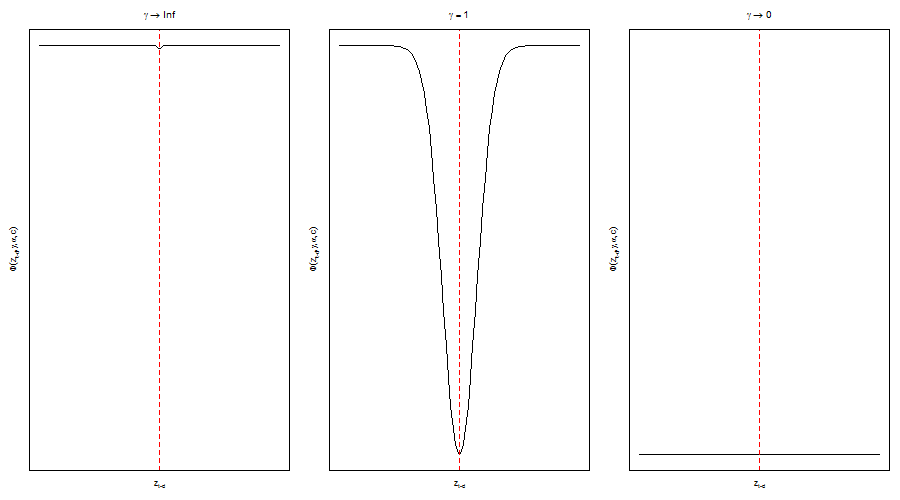

- 2 Exponential STAR:

\[ G(z_t)=1-e^{-\gamma(z_t-c)^2} \]